")

")

Thailand Energy Report 2015

Thailand Energy Report 2015

“In 2015, Energy production in Thailand decreased, resulting in more imports to meet domestic demand. The final energy consumption increased by 4.0% because the Thai economy started to recover (GDP grew by 2.8%) while the energy prices are in a downtrend due to the oversupply of oil, natural gas and coal in the world market. The prices of Diesel, Gasoline and Gasohol increased from the low level. The jet fuel consumption increased by the number of foreign tourists. The foreign Tourists were 29.9 million increases about 5 million people compare to previous year. The electricity consumption increased because the longer period of hot weather occurred and the expansion of the business sector is another key factor that affected the increasing electricity consumption in 2015.

The commercial primary energy production was at 1,026 thousand barrels of oil equivalent per day, down by 4.3%. Production of lignite decreased due to the reduction of Mae Moh power plant and industrial sectors demand. The hydroelectric decreased as well from the decreased of water reserve and the lower rain fall compared to the same period last year.

The net primary energy imported stood at 1,251 thousand barrels of oil equivalent per day. It is increase by 6.8%. The net import of energy was increased, In particular, the electricity imported that increased because the starting of electric supply from Hongsa power plant in Lao PDR., in February 2015. The import of natural gas increased since August 2014 by the selling of natural gas from the Zortica in Myanmar together with the increasing of LNG imports.

The final energy consumption was 1,420 thousand barrels of oil equivalent per day, or 4.0% up, according to Thailand's economy grew at 2.8%. it is a result of government stimulus policies that enhance the consumption and investment within the country. The 54% share of final energy

consumption is for petroleum products.

The value of energy imported was at 912,931 million baht, down 34.8%. The main factor that reduced energy imported value is the low of crude oil prices (crude oil has 65% share of the total Thailand energy imports) and the average price of imported crude oil in Thailand was at 54.3 US $ / BBL in 2015. The imported value of all kinds of energy reduced due to the reduction of energy prices except electricity and LNG imports increased because the expansion of imported volumes.

The value of energy exports stood at 218,472 million baht, down 31.3%, due in no crude exports from September 2557 to November 2558 in accordance with government policy.In December 2558, it began exporting crude oil from the Wassana Resource because the refineries in the country cannot be refined. The exported petroleum product price was lower compared to the previous year.

Energy Prices

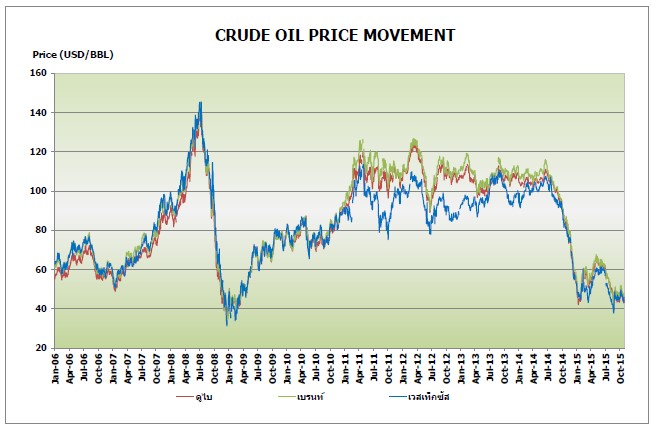

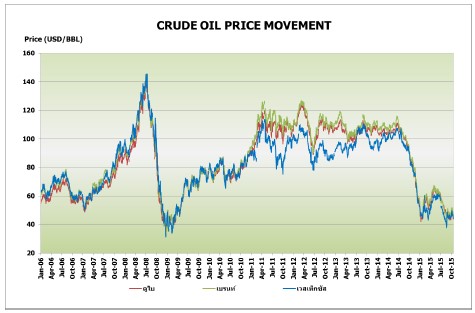

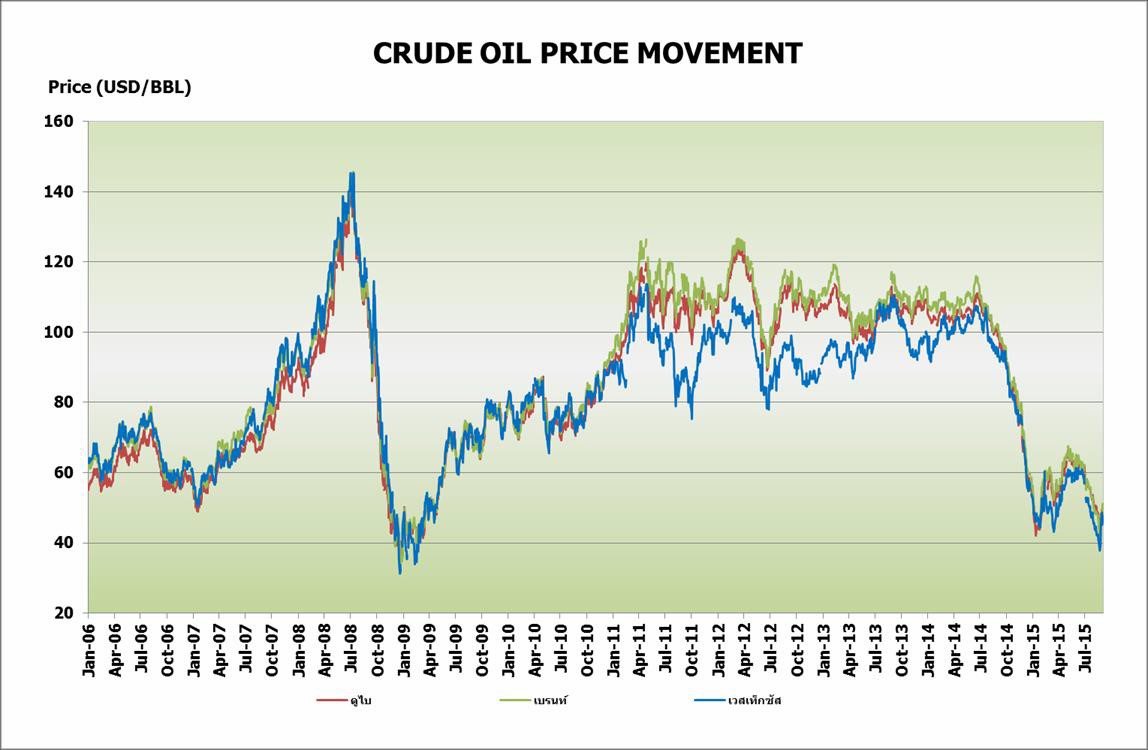

Dubai crude oil price in December 2015 is averaged at 34.6 USD / BBL but the average price of 2015 was at 50.8 USD / BBL. The crude oil price was fluctuated because of the over oil supply that was affected by the slowdown of global economy growth and the levelize of oil production to maintain the market share of OPEC and Russia aAnd the El Nino phenomenon, resulting in temperatures in the Northern Hemisphere, higher than normal levels in the winter.

In December 2015, gasoline retail prices in the ASEAN region fell by almost countries except Brunei that has fixed prices. The retail price of diesel dropped by the whole region.

The price of LPG (CP) in December 2015 was 466 US $ / ton increase from the previous month in November 2015, which is at 411 US $ / ton. The retail price of LPG in the month of December 2015 stood at 22.29 baht / kg. This price was freeze in order to low down effect of the cost of living.

LNG prices in the world market dropped from oversupply in the world market and as a result of the weather in the East are not very cold, like every year. The oil price is low so it was used to replace some LNG in some country.

Crude oil supply is 1,028 thousand barrels per day by 85% of imports. The 8.8% increase in imports, mainly from Middle East countries. The rest is domestic production rose 10.0%, the refining capacity of the country stood at 1,252 thousand barrels per day. Crude was used in Refining for 90% of the refining capacity..

Petroleum products consumption is at 132 million liters per day, up 4.3%.

The diesel consumption is at 60.1 million liters per day accounted for 46% of all petroleum products. It is increased 4.1% by the prices reduction.

The consumption of gasoline and diesel fuel was at 26.4 million liters per day. Accounted for 20% of all petroleum products consumption. The demand rose to 13.2% due to the low oil prices that encourage the auto LPG and NGV users turning to use more oil because it is cheaper and more convenient evenly over the service station.

Jet fuel consumption was at 16.5 million liters per day, up 9.4% from the expansion in tourism sector. In 2015, the foreign tourists come to visit at 29.9 million people, up from about 5 million from the years ago.

The LPG consumption was at 6,695 thousand tons, down 10.9%, the consumption of LPG in several sector will be described as follow;

Petrochemical industry (As raw material) accounted for most of the 32% decrease of 20.6% from the slowdown of downstream industries and the export sector is still shrinking.

Households sector accounted for 31%, down 4.3%, it was a result from the adjusting retail LPG prices structure to reflect actual costs, that effected the prices in household sector higher than the last year prices so there was no motive to smuggle LPG.

Automobile consumption fell 12.3% due to lower oil prices resulting that some users turn to oil instead of LPG.

Industry consume 3.0% up compared to the previous year by adjusting the price to equal the household and transportation sector price.

The refineries self-consumption increased to 50.6% due to excess LPG from other sector.

Natural Gas

The natural gas consumption was at 4764 million cubic feet per day, up by 2.0%. It is increased 4.3% for electricity generation (share of NG for electricity generation is about 60%) while the consumption of NG in other sector were slowdown especially in the consumption as NGV that decreased by 4.1% from the price increased from last year. Another factor that affected to decrease NG consumption is the decreasing of oil price. The fell down of oil price and some limitation of NGV service station make some of NGV car owner convert their engine to use oil instead of NGV. There are only 500 NGV stations in the whole country at the end of December 2015.

Lignite / Coal

The supply of lignite / coal was at 37.1 million tons, down by 4.7% compared to previous year. Lignite production decreased by 15.7% from the domestic demand reduction. While imports of coal increased 4.8% by the increasing of the industrial sector consumption.

- The lignite consumption was at 15.1 million tons, down 17.8%. This is because of the decreasing in electricity production of Mae Moh power plant that was affected by limitations of the transmission line. Another reason was the feeding electricity in the transmission system of Hongsa power plant in February 2015 and the decreased of electricity consumption in the industrial sector.

The imported coal consumption was at 21.9 million tons, up 5.0%. The consumption is mainly in the industrial sector, which rose 11.4%, to replace lignite. While the imported coal consumption decreased in electric generation sector.

Electricity

The generation power in the electrical system at the end of December 2015 was at 38,815 MW (excluding the production of electricity from power plants VSPP). The EGAT has a maximum production capacity (40%), followed by the IPP (38 %), SPP (13%) and import / foreign exchange (9%).

Electricity production was at 192,189 GWh (including the generation from VSPP) increased 3.3%. The fuels used to produce electricity are natural gas (67%), renewable energy (5%). The Production of electricity by RE increased 10.4% compared to last year. This is because of the promotion of RE in electricity generation of Ministry of Energy.

The Net Peak Generation Requirement occurred at 27,346 MW on Thursday, June 11, 2015 at 14:02 hrs. It is up 1.5% compared to last year, due to the hot weather for a long time, resulting in peak shift from April or May to be June this year.

Power consumption was 174,834 GWh, increased 3.7% from the hot weather, and the expansion of the business sector especially in Tourism and construction sector. While the electricity consumption in the industrial sector was slowly increase because of a contraction of exports that impacted by the low expansion of global economy. Also the electricity consumption increased by nearly all economic sectors except for use in agriculture decreased due to serere drought.

CO2 emissions in energy consumptions

In 2015, a CO2 emission from energy consumption was at 254 million tons of CO2 increased by 1.6%. CO2 emissions came from the transportation, industrial and other economic sectors (including households, agriculture and commerce), while the CO2 emissions is reduced in electricity production. The CO2 emissions per energy consumption was at 1.96 tons of CO2 per KTOE. It is lower than the world average in 2013, which stood at 2.40 tons of CO2 per KTOE.

Data as of March 10, 2016

The energy situation in the first tenth months of 2015 and outlook for 2015

The energy situation in the first tenth months of 2015 and outlook for 2015

Office of Economic and Social Development Board (NESDB) forecasted that Thailand's economy in the 3rd quarter of 2015 will grow by 2.9 percent compared to the GDP growth in Q2 (Q2. the economy grew 2.8 per cent).

The expansion in agricultural manufacturing and export sectors are likely to be lower than expected but there are still driven by the tourism sector. Tourist is expected to arrive in the country up to 30 million people throughout the year.

However, Thailand's economy this year has been affected by drought and the global economic recovery continues to be delayed. The price of crude oil imports in 2015 was lower down. As a result, export prices on world markets fell. It forecasts that the average Dubai crude oil price in 2015 is at 52.5 USD per barrel lower than the assumption price of the forecast (Assuming that 50 - 60 USD per barrel).

The economic outlook for Thailand in 2016, NESDB. Is expected that it will expand by 3.0 - 4.0 percent by Government spending and public investment Including the stimulus and the recovery of global economic.

EPPO, Predicted that the final energy consumption in 2016 is expected to rise to 2.7 - 3.5 percent due to the economic recovery and oil prices remain low. This is consistent with the NESDB economic forecasted that Thailand's economy will expand by 3.0 - 4.0 percent

Electricity consumption in the first 10 months of 2015.

In the first 10 months of 2015, electricity consumption is expected to be 145,760 Gigawatt-hour Increased 3.2 percent because of the prolonged period of hot weather, the expansion of the business sector, especially tourism, business services and construction. Electricity consumption increased in almost every sectors except the agricultural sector that the consumption decline because of drought. The industrial sector accounts for the peak load representing 43 percent of total use. Electricity consumption has increased by 1.0 percent compared to the same period last year. The consumption of electricity in Household account for 24 percent of the total 5.2 percent increase in consumer spending due to the increase attributed to the hot weather. The small enterprises consumption and electrical appliances consumption have increased by 5.5 and 4.6 percent respectively.

Net Peak Generation Requirement in EGAT System was occurred at the temperature of 36.7 degrees Celsius on Thursday 11 June 2015 at 14.02 hrs. at 27 346 megawatts. It is higher than the Peak of the year which occurred on Wednesday, April 23, 2014 at 14:26 hrs. at 404 MW, an increase of 1.5 percent.

The predicted peak of the year 2016, EPPO, predicted Peak in two cases: 1) Base Case forecasts the Peak at 28,300 MW 2) If the temperature rises 3 degrees Celsius. predicted Peak was at 29,000 megawatts, the ministry has set up a surveillance at 28,500 megawatts.

The projected value Peak in the year 2016, if temperatures rise by 3 degrees Celsius, the expected value Peak is located at 29,000 MW, which is higher than the level of surveillance of the energy required by the government is taking measures to reduce the Maximum peak Demand by the following measures;

1) Measures “Demand Respond”

2) Measures Campaign "Energy divided by two."

3) Measures “Changed by high performance device”

FT during September - October 2015 stood at 46.38 satang per unit, down 3.23 satang per unit compared with the May - August 2015. In November 2015, the electricity bill will be restructured so the FT from November 2558 will be stood at -3.23 satang per unit.

The tariff formulated by automatically tariff adjustment formula (Ft).

- Unit: Satang/unit

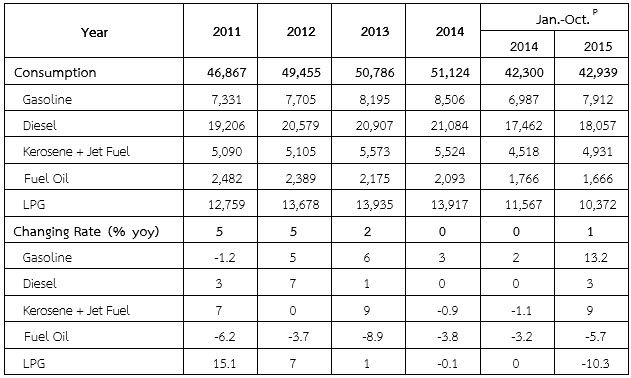

In the first ten months of 2015, the petroleum products consumption was increased 1.5 percent. The demand of gasoline rose 13.2 percent due to a decrease of domestic gasoline retailed price which was affected by the decline in oil prices in the world market. The expansions of the tourism sector make diesel and jet fuel consumption increased by 3.4 and 9.2 percent respectively. Use of fuel oil dropped 5.7 percent.

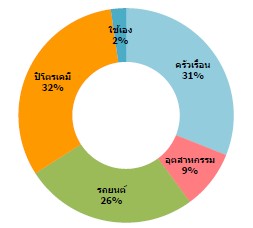

The LPG consumption in the first ten months of 2015 has decreased by 10.3 percent due to lower demand in the high energy consumption proportion economic sector. Consumption in the petrochemical sector which has the highest proportion (32 percent) has decreased by 19.5 percent. In the households sector (with 31 percent share), The LPG consumption have decreased by 4.6 percent and steadily declined since the start of stringent measures to suppress the illegal distribution of LPG misuse. LPG consumption in transportation sector (26 percent share) have decreased 11.4 percent due to an increase in LPG prices, as oil prices fell, some turn to make use of petroleum fuel, instead of using LPG. While the industrial sector has increased LPG demand by 3.7 percent.

Petroleum Products Consumption

Unit: million liters

Remark /Pestimated from data as of September 2015

LPG include the utilized as feed stock of petrochemical

LPG, Propane and Butane Consumption

Unit: thousand tons

Remark /Pestimated from data as of October 2015

สัดส่วนการใช้ LPG ม ค -ต ค 2558

Fuel consumption for land transport

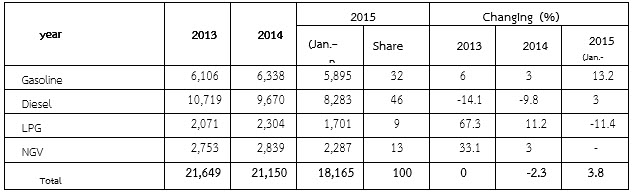

In the first 10 months of 2015, the fuel consumption in land transport sector stood at 18,165 kilo tons of oil equivalent (ktoe) increase over the same period of the previous year by 3.8 percent. It is caused by an increase in the use of gasoline and diesel. The diesel (Holds up to 46 percent of energy use in all sectors of land transport) has increased by 3.4 percent compared to the same period last year.While the uses of LPG and NGV in the car (9 and 13 percent, respectively) are down 11.4 and 3.3 percent, respectively, this is a major cause of the decline in prices. Gasoline and diesel steadily since mid-2014, and the price hike of LPG and NGV in 2014 for restructuring policies to reflect the true cost of government. The average retail price of LPG and NGV in the transport sector rose 2.08 and 2.45 baht per kg. The limitations of NGV service stations that still is not enough to make the use of LPG and NGV partial return to the oil.

In the first 10 months of 2015, the average retail price of LPG and NGV is at 23.55 and 13.05 baht per kilogram), up 2.08 and 2.45 baht per kilogram, respectively, compare to the same period last year. While the cumulative NGV car is at 471.392, increase 2.6 percent, in October 2015. The NGV service stations at the end of October 2015 totaled 500 stations, up from the previous year, only 4 stations.

The Energy Consumption in Land Transportation Sector

unit : ktoe

Remark /Pestimated from data as of October 2015

Price and value of Energy Import

Crude oil prices (The average price of Dubai) during October 2015 was at $46.02 a barrel, up 0.64 US dollars per barrel compared to the average price in September 2015 due to the concerns over supply condition.

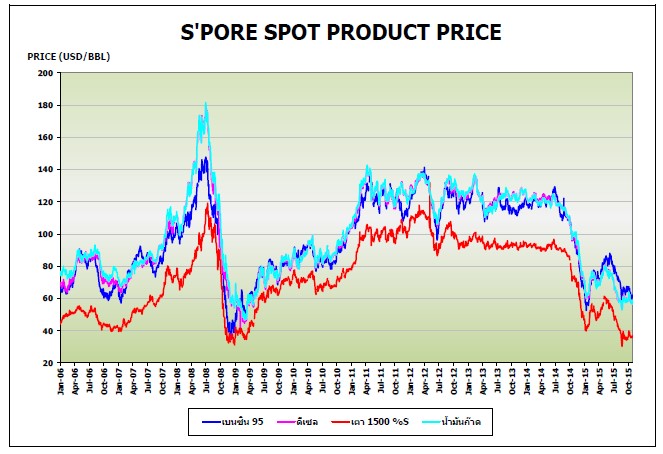

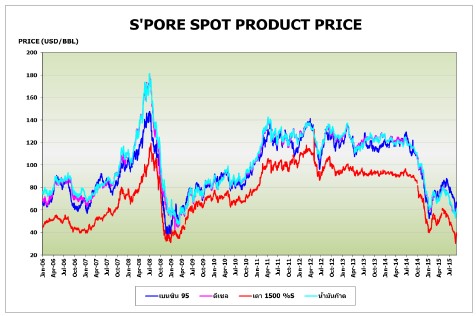

The price of gasoline and diesel fuel (average price in Singapore market) during the month of October 2015 was at US $ 63.54 a barrel, down 1.70 US dollars per barrel compared to the average price in the previous month due to inventory is high. While diesel averaged price is at US $ 59.21 a barrel low down 0.27 US dollars per barrel due to increasing of demand from the starting operation of oil refinery. However, diesel prices fell less than the price of gasoline due to increased demand from Asian countries.

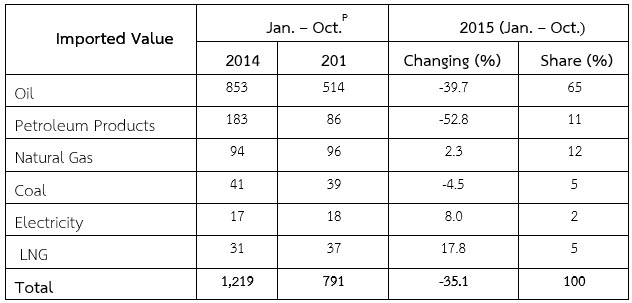

The total energy imported value during the first 10 months of 2015 was estimated at 791 billion baht, down 35.1 percent compared to the same period in 2014 due to a decrease in the price of imported energy. The import value of each type of energy is reducing. Except natural gas, electricity and liquefied natural gas (LNG) imports are increasing as the volume of imports. The value of imports increased by 17.8, 8.0 and 2.3 percent, respectively. The value of crude oil imported fell 39.7 percent according to crude oil price in the world market. The reduction of coal prices in the world market make the coal imported value fell by 4.5 percent compared to the same period last year. The value of imported petroleum products is down 52.8 percent due to the reduction of petroleum products volume and prices.

Energy Imported Value

Unit: billion Baht

Remark /P estimated from data as of October 2015

Energy Forecast and Information Technology Center

Energy Policy and Planning Office

November 24, 2015

The energy situation in the first nine months of 2015 and outlook for 2015

The energy situation in the first nine months of 2015 and outlook for 2015

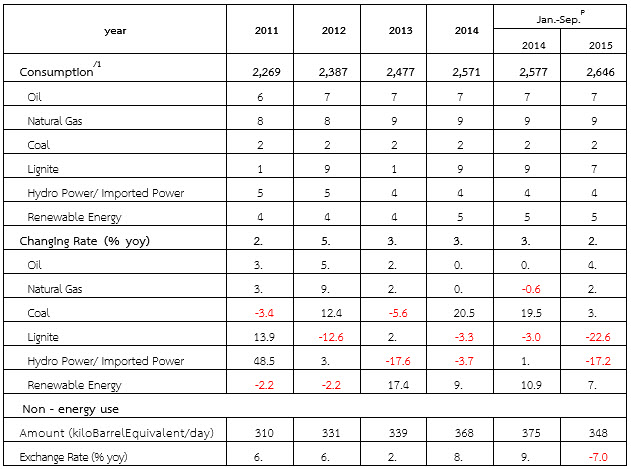

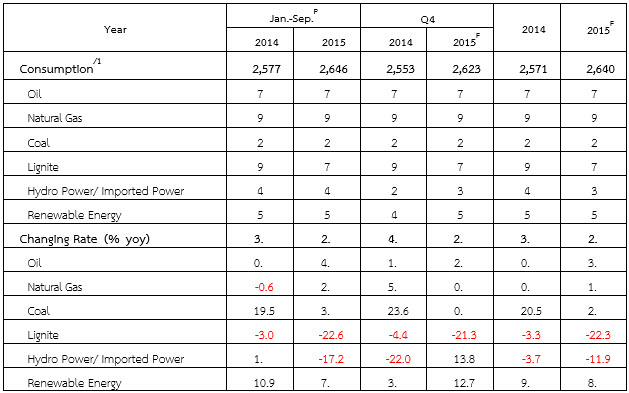

During the first nine months of 2015, the primary energy consumption is expected to be 2,646 thousand barrels of oil equivalent per day, increase from the same period in 2014 by 2.7 percent. Oil consumption is expected to increase by 4.1 percent as oil prices are likely to decrease. The natural gas consumption is expected to increase by 2.4 percent due to the increasing of power generation by Independent Power Producers (IPP) and Small Power Producer (SPP). The coal consumption is expected to increase by 3.8 percent since been used in industry for the replacement of lignite that was decreased by constraints of volume production of lignite in the country. The consumption of lignite is expected to fall 22.6 percent compared to the same period last year. This is because of the shutdown for maintenance of lignite power plant and the reducing in electricity production of the Mae Moh power plant to make the transmission system more capacity for the synchronize testing of Hongsa power plant. The hydropower and electricity imports consumption are expected to decline 17.2 percent due to low rainfall over the past few years. This cause the amount of water used to produce electricity low. The renewable energy consumption is expected to rise 7.3 percent.

Primary Energy Consumption

Unit: kilo barrels of oil equivalent per day

Remark /1 not include Non – Energy use

/Pestimated from data as of September 2015

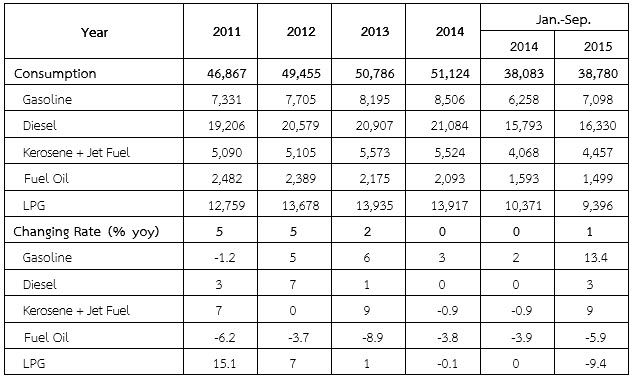

In the first nine months of the year 2015, the petroleum products consumption was at 142 million liters per day increased 1.8 percent. The demand of gasoline rose 13.4 percent due to a decrease of domestic gasoline the retail price which was affected by the decline in oil prices in the world market. The expansions of the tourism sector make diesel and jet fuel consumption increased by 3.4 and 9.6 percent respectively. Use of fuel oil dropped 5.9 percent from its use as a fuel to produce electricity.

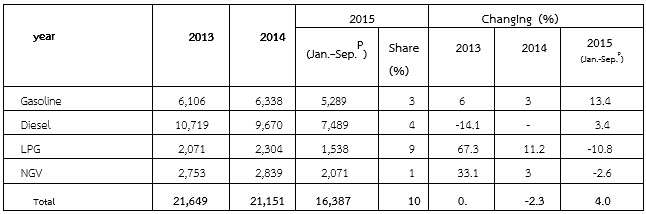

The LPG consumption in the first nine months of 2015 has decreased by 9.4 percent due to lower demand in the high energy consumption proportion economic sector. Consumption in the petrochemical sector which has the highest proportion (32 percent) have decreased by 17.2 percent. In the households sector (with 31 percent share), The LPG consumption have decreased by 4.9 percent and steadily declined since the start of stringent measures to suppress the illegal distribution of LPG misuse. LPG consumption in transportation sector (26 percent share) have decreased 10.8 percent due to an increase in LPG prices, as oil prices fell, some turn to make the use of petroleum fuel, instead of using LPG. While the industrial sector has increased LPG demand by 3.8 percent.

Petroleum Products Consumption

Unit: million liters

Remark LPG include the utilized as feed stock of petrochemical

LPG, Propane and Butane Consumption

Unit: thousand tons

Fuel consumption for land transport

In the first nine months of 2015, the fuel consumption in land transport sector stood at 16 386 kilo tons of oil equivalent (ktoe) increase over the same period of the previous year by 4.0 percent. It is caused by an increase in the use of gasoline and diesel. The diesel (Holds up to 46 percent of energy use in all sectors of land transport) has increased by 3.4 percent compared to the same period last year.While the uses of LPG and NGV in the car (13 and 9 percent, respectively) are down 10.8 and 2.6 percent, respectively, this is a major cause of the decline in prices. Gasoline and diesel steadily since mid-2014, and the price hike of LPG and NGV in 2014 for restructuring policies to reflect the true cost of government. The average retail price of LPG and NGV in the transport sector rose 2.38 and 2.50 baht per kg. The limitations of NGV service stations that still is not enough to make the use of LPG and NGV partial return to the oil.

The current retail price of LPG and NGV is at 22.29 and 13.50 baht per kilogram (Approved by the Board of Directors Energy Policy Administration on September 8, 2015), while the number of NGV service stations at the end of September 2015 totaled 500 stations, up from the previous year, only 4 stations.

The Energy Consumption in Land Transportation Sector

unit : ktoe

Remark /P estimated from data as of September 2015

The production and consumption of electricity during the first nine months of 2015

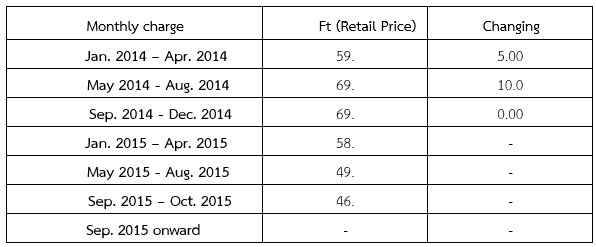

FT during September - October 2015 stood at 46.38 satang per unit, down 3.23 satang per unit compared with the May - August 2015. In November 2015, the electricity bill will be restructured so the FT from November 2558 will be stood at -3.23 satang per unit.

The electricity consumption during the first nine months of the year 2015is approximated to be 130,800 gigawatt hours. It is increased 3.2 percent due to the hot weather in the summer and rainfall slower than last year. The electricity utilization increased in almost all sectors except agriculture.

The tariff formulated by automatically tariff adjustment formula (Ft).

Unit: Satang/unit

Price and value of Energy Import

Crude oil prices (The average price of Dubai) during the month of September 2015 stood at US $ 45.38 a barrel, down 2.32 US dollars per barrel compared to the average price in the month of August 2015 due to the concerns over supply condition.

The price of gasoline and diesel fuel (average price in Singapore market) during the month of September 2015 is at US $ 65.24 a barrel, down 0.74 US dollars per barrel compared to the average price in the previous month due to inventory is high. While diesel averaged price is at US $ 59.48 a barrel rose 2.44 US dollars per barrel due to increased demand from China, Vietnam, Myanmar and West Africa and several refineries were shut down for maintenance.

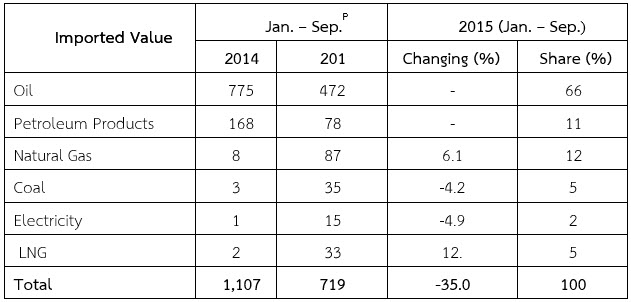

The total energy imported value during the first 9 months of 2015 was estimated at 719 billion baht, down 35.0 percent compared to the same period in 2014 due to a decrease in the price of imported energy. The import value of each type of energy is reduction. Except natural gas and liquefied natural gas (LNG) imports are increasing as the volume of imports. The value of imports increased by 12.2 and 6.1 percent, respectively. The value of crude oil imported fell 39.2 percent according to crude oil price in the world market. The reduction of coal prices in the world market make the coal imported value fell by 4.2 percent compared to the same period last year. The value of imported petroleum products is down 53.6 percent due to the reduction of petroleum products volume and prices. The electricity imported value decreased 4.9 % by the reduction of imported volume.

Energy Imported Value

Unit: billion Baht

Remark /P estimated from data as of September 2015

Trends in energy consumption in 2015

Primary energy demand forecast for the fourth quarter of 2015 is estimated at 2623 thousand barrels of oil equivalent per day increase of 2.8 percent compared to the same period in 2014. It is expected that there will be increased demand for each kind of energy except the lignite consumption is expected to decrease as domestic production volumes of lignite continues steadily declined. It expected at 21.3 percent demand reduction. Oil consumption is expected to increase by 2.7 percent as oil prices are likely to stay low. It is because of the expansion in tourism sector. It affected that gasoline, diesel and jet fuel consumption has increased as well as the first nine months of 2015. Natural gas consumption during the fourth quarter of 2015 is expected to increase by 0.4 percent. Hydropower / electricity imports are expected to have a 13.8 percent increase. This is because the increasing of electricity imports by the commercial commissioning of Hongsa Power Plant Unit 2 in November 2015. While the use of coal in the fourth quarter of 2558 is expected to increase slightly. (increase 0.1 percent compared to the same period of 22014) and the renewable energy is expected to increase at 12.7 percent by the enhancing renewable energy utilization policies of Ministry of Energy.

The primary energy consumption in 2015 is estimated at 2,640 thousand barrels of oil equivalent per day increase 2.7 percent compared with the year 2014. It expand according to the 2015 economic growth. Predicts that the use of oil for the year 2558 will increase by 3.7 percent for gasoline, diesel and jet fuel. The use of natural gas will increase by 1.9 percent and the coal consumption is expected to increase at 2.8 percent to replace the need of lignite in industrial sector. It is expected that the lignite consumption in 2015 will be down to 22.3 percent based on the decline production volumes by the private of lignite mining and manufacturer. The maintenance of Mae Moh power plant and limitations of the transmission system after the synchronize of Hongsa power plant will decrease the consumption of lignite too. While the use of hydropower and electricity imports are expected to decline 11.9 percent from hydroelectric power drop during the dry season and the less rain fall in 2015. In the year 2015, the renewable energy consumption is expected to increase by 8.6 percent compared to the previous year.

The petroleum products consumption in 2015 is expected to increase by 1.2 percent. The gasoline consumption increased by 12.5 percent due to the drop in gasoline prices, especially in the first half, by the decreasing of gasoline average retail price that affected to rise up the consumption of gasoline to 14.0 percent For diesel, are expected to have increased by 3.3 percent and jet fuel rose 8.1 percent based on the expansion of the tourism sector.

The LPG consumption in 2015 is estimated to have decreased 10.7 percent due to lower demand for household use in the transportation sector and the petrochemical industry. Using the car is expected to decline 11.9 percent due to an increase in LPG prices, as oil prices fell, some turn to make the use of LPG instead of gasoline. The household sector decreased by 4.1 percent. For use in the petrochemical industry is expected to have decreased by 20.6 percent due to the impact of the export slowdown while the manufacturing sector is estimated to have increased by 3.4 percent due to lower prices on the market.

Electricity consumption in 2015 is expected to have a power rating of 173 862 GWh increased 3.1 percent compared to the year 2014. This because the increasing of electricity consumption in almost economic sector except for agriculture which has been affected by drought.

Estimated Primary Energy Consumption

Unit : Kilo Barrel of Oil Equivalent/day

หมายเหตุ /1Not include Non – Energy use

/Pestimated from data as of September 2015

/Festimated from data as of 4th semester of 2015

Energy Forecast and Information Technology Center

Energy Policy and Planning Office

October 28, 2015

The energy situation in the first eight months of 2015 and outlook for 2015

The energy situation in the first eight months of 2015

Thailand’s economic forecast 2015 by the Office of Economic and Social Development Board (NESDB.) point out that Thailand's economy is expanding in the range of 2.7 to 3.2 percent due to the acceleration of government spending and investment and the implementation of public investment. The oil prices and inflation are likely to remain low, it will help increase the real purchasing power of the people. However, the slowdown of the global economy, especially China, and the Ratchaprasong Explosion on August 17, 2015 that could affect the confidence of tourists there are also risks to the growth of Thai’s economy. It is expected that the average Dubai crude oil price in 2015 is in the range of 40.0 to 45.0 US dollars per barrel.

During the first eight months of 2015, the primary energy consumption is expected to be 2,603 thousand barrels of oil equivalent per day, increase from the same period in 2014 by 2.4 percent. Oil consumption is expected to increase by 4.0 percent as oil prices are likely to decrease. The natural gas consumption is expected to increase by 1.9 percent due to the increasing of power generation by Independent Power Producers (IPP) and Small Power Producer (SPP). The coal consumption is expected to increase by 4.0 percent due to their used in industry for the replacement of lignite that was decreased by constraints of volume production of lignite in the country. The consumption of lignite is expected to fall 21.6 percent compared to the same period last year. This is because of the shutdown for maintenance of lignite power plant and the reducing in electricity production of the Mae Moh power plant to make the transmission system more capacity for the synchronize testing of Hongsa power plant. The hydropower and electricity imports consumption are expected to decline 19.2 percent due to low rainfall over the past few years. This cause the amount of water used to produce electricity to be low. The renewable energy consumption is expected to rise 7.3 percent.

Primary Energy Consumption

Unit: kilo barrels of oil equivalent per day

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Remark/Pestimated from data as of August 2015

In the first eight months of 2015, the petroleum products consumption increased 2.2 percent. The demand of gasoline rose 13.3 percent due to the decrease of domestic gasoline retail price which was affected by the decline in oil prices in the world market. The expansions of the tourism sector make diesel and jet fuel consumption increased by 3.3 and 9.1 percent respectively. Use of fuel oil dropped 6.6 percent.

The LPG consumption in the first eight months of 2015 has decreased by 7.7 percent due to lower demand in transport, Household and petrochemical sector. LPG consumption in transportation sector have decreased 9.5 percent due to the increase of LPG prices, as oil prices fell, some customers turn to petroleum oil instead of LPG. In the household sector, The LPG consumption have decreased by 4.8 percent and steadily declined since the start of stringent measures to suppress the illegal distribution of LPG. While the industrial sector has increased LPG demand by 4.7 percent.

Petroleum Products Consumption

Unit: million liters

|

Year |

2011 | 2012 | 2013 | 2014 | Jan.-Sep.P | |

| 2014 | 2015 | |||||

| Consumption | 46,867 | 49,455 | 50,786 | 51,124 | 34,022 | 34,766 |

| Gasoline | 7,331 | 7,705 | 8,195 | 8,506 | 5,550 | 6,291 |

| Diesel | 19,206 | 20,579 | 20,907 | 21,084 | 14,182 | 14,657 |

| Kerosene + Jet Fuel | 5,090 | 5,105 | 5,573 | 5,524 | 3,660 | 3,994 |

| Fuel Oil | 2,482 | 2,389 | 2,175 | 2,093 | 1,433 | 1,338 |

| LPG | 12,759 | 13,678 | 13,935 | 13,917 | 9,196 | 8,487 |

| Changing Rate(%yoy) | 5.6 | 5.5 | 2.7 | 0.7 | -0.01 | 2.2 |

| Gasoline | -1.2 | 5.1 | 6.4 | 3.8 | 1.1 | 13.3 |

| Diesel | 3.8 | 7.1 | 1.6 | 0.8 | 0.3 | 3.3 |

| Kerosene + Jet Fuel | 7.7 | 0.3 | 9.2 | -0.9 | -0.1 | 9.1 |

| Fuel Oil | -6.2 | -3.7 | -8.9 | -3.8 | -3.8 | -6.6 |

| LPG | 15.1 | 7.2 | 1.9 | -0.1 | -0.5 | -7.7 |

Remark/Pestimated from data as of August 2015

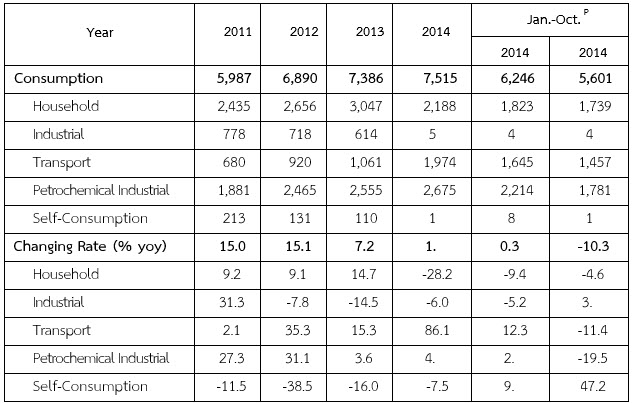

Fuel consumption for land transport

In the first eight months of 2015, the fuel consumption in land transport sector stood at 14,656 kilo tons of oil equivalent (ktoe) increase over the same period of the previous year by 4.3 percent. It is caused by an increase in the use of gasoline and diesel. The diesel (Holds up to 46 percent of energy use in all sectors of land transport) has increased by 3.3 percent compared to the same period last year.While the uses of LPG and NGV in the car (9 and 13vpercent, respectively) are down 9.6 and 1.3 percent, respectively, this is a major cause of the decline in prices. Gasoline and diesel steadily since mid-2014, and the price hike of LPG and NGV in 2014 for restructuring policies to reflect the true cost of government. The limitations of NGV service stations that still is not enough to make the use of LPG and NGV partial return to the oil.

In the first eight months of 2015, the average retail price of LPG and NGV is at 23.92 and 12.94 baht per kilogram), up 2.54 and 2.44 baht per kilogram, respectively, compare to the same period last year. While the cumulative NGV car is at 470,565, increase 3.5 percent, in August 2015. The NGV service stations at the end of August 2015 totaling 499 stations, up from the previous year, only 3 stations.

The Board of Energy Policy Administration on September 8, 2015 approved retail price of LPG and NGV at 22.29 and 13.50 baht per kilogram, respectively

The Energy Consumption in Land Transportation Sector

unit : ktoe

|

year |

2013 |

2014 |

2015 | Changing(%) | |||

| (Jan.–Sep.P) | Share(%) | 2013 | 2014 |

2015 (Jan.-Sep.P) |

|||

| Gasoline | 6,106 | 6,338 | 4,687 | 32 | 6.4 | 3.8 | 13.3 |

| Diesel | 10,719 | 9,670 | 6,722 | 46 | -14.1 | -9.8 | 3.3 |

| LPG | 2,071 | 2,304 | 1,382 | 9 | 67.3 | 11.2 | -9.6 |

| NGV | 2,753 | 2,839 | 1,866 | 13 | 33.1 | 3.1 | -1.3 |

| Total | 21,649 | 21,150 | 14,656 | 100 | 0.6 | -2.3 | 4.3 |

Remark /Pestimated from data as of August 2015

The production and consumption of electricity during the first eight months of 2015

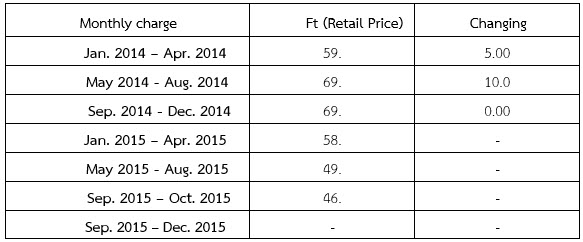

FT during May - August 2015 stood at 49.61 satang per unit, will be down 3.23 satang per unit in the September - December 2015 due to the drop of fuel prices in the world market, and the depreciate of exchange rate in the past.

The electricity consumption during the first eight months in 2015is approximated 116,350 gigawatt hours. It is increased 3.4 percent due to the hot weather in the summer and rainfall slower than last year. The electricity utilization increased in almost all sectors except agriculture.

The tariff formulated by automatically tariff adjustment formula (Ft).

Unit: Satang/unit

| Monthly charge | Ft(Retail Price) | Changing |

| Jan. 2014–Apr. 2014 | 59.00 | 5.00 |

| May 2014-Aug. 2014 | 69.00 | 10.00 |

| Sep. 2014-Dec. 2014 | 69.00 | 0.00 |

| Jan. 2015–Apr. 2015 | 58.96 | -10.04 |

| May 2015-Aug. 2015 | 49.61 | -9.35 |

| Sep. 2015–Oct. 2015 | 46.38 | -3.23 |

Price and value of Energy Import

Crude oil prices (The average price of Dubai and West Texas) during August 2015 stood at US $ $47.69 and $42.77a barrel, down $8.47 and $8.12US dollars per barrel, respectively, compared to the average price in July 2015 due to the concerns over supply condition.

The price of gasoline and diesel fuel (average price in Singapore market) during August 2015 is at $65.98 and $57.04, down $9.97 and $8.04 per barrel compared to the average price in the previous month.

The total energy imported value during the first 8 months of 2015 was estimated at 654 billion baht, down 33.3 percent compared to the same period in 2014 due to a decrease in the price of imported energy. The import value of each type of energy is reduction. Except natural gas and liquefied natural gas (LNG) imports are increasing as the volume of imports. The value of imports increased by 11.7and 8.6 percent, respectively. The value of crude oil imported fell 36.7 percent according to crude oil price in the world market. The reduction of coal prices in the world market make the coal imported value fell by 5.9 percent compared to the same period last year. The value of imported petroleum products is down 53.8 percent due to the reduction of petroleum products volume and prices. The electricity imported value decreased 8.0 % by the reduction of imported volume.

Energy Imported Value

Unit: billion Baht

|

Imported Value |

Jan. – Aug.P | 2015(Jan. – Aug.) | ||

| 2014 | 20158 | Changing(%) | Share(%) | |

| Oil | 683 | 432 | -36.7 | 66 |

| Petroleum Products | 153 | 71 | -53.8 | 11 |

| Natural Gas | 70 | 78 | 11.7 | 12 |

| Coal | 33 | 31 | -5.9 | 5 |

| Electricity | 13 | 12 | -8.0 | 2 |

| LNG | 28 | 30 | 8.6 | 5 |

| Total | 980 | 654 | -33.3 | 100 |

Remark /P estimated from data as of August 2015

Energy Forecast and Information Technology Center

Energy Policy and Planning Office

October 28, 2015

กบง. ครั้งที่ 22 - วันจันทร์ที่ 2 พฤษภาคม พ.ศ. 2559

มติการประชุมคณะกรรมการบริหารนโยบายพลังงาน

ครั้งที่ 10/2559 (ครั้งที่ 22)

เมื่อวันจันทร์ที่ 2 พฤษภาคม 2559 เวลา 13.30 น.

1. โครงสร้างราคาก๊าซ LPG เดือนพฤษภาคม 2559

2. แผนระบบรับส่งและโครงสร้างพื้นฐานก๊าซธรรมชาติเพื่อความมั่นคง

ผู้มาประชุม

1. รัฐมนตรีว่าการกระทรวงพลังงาน ประธานกรรมการ

(พลเอก อนันตพร กาญจนรัตน์)

8. ผู้อำนวยการสำนักงานนโยบายและแผนพลังงาน กรรมการและเลขานุการ

(นายทวารัฐ สูตะบุตร)

เรื่องที่ 1 โครงสร้างราคาก๊าซ LPG เดือนพฤษภาคม 2559

สรุปสาระสำคัญ

1. คณะกรรมการบริหารนโยบายพลังงาน (กบง.) เมื่อวันที่ 7 มกราคม 2558 และเมื่อวันที่ 3 เมษายน 2558 ได้เห็นชอบการกำหนดหลักเกณฑ์การคำนวณราคา ณ โรงกลั่น ซึ่งเป็นราคาซื้อตั้งต้นของก๊าซ LPG โดยใช้ต้นทุนจากแหล่งผลิตและแหล่งจัดหา (โรงแยกก๊าซธรรมชาติ โรงกลั่นน้ำมันเชื้อเพลิงและโรงอะโรเมติก นำเข้า และ ปตท.สผ.) เฉลี่ยแบบถ่วงน้ำหนักตามปริมาณการผลิตและจัดหาเฉลี่ยย้อนหลัง 3 เดือน ทั้งนี้ให้มีการทบทวนราคาต้นทุนจากแหล่งผลิตและแหล่งจัดหาทุกๆ 3 เดือนดังนั้น ฝ่ายเลขานุการฯ จึงได้มีการทบทวนต้นทุนจากแหล่งผลิตและแหล่งจัดหา โดยมีรายละเอียด ดังนี้ (1) ต้นทุนจากโรงแยกฯ เดือนพฤษภาคม-กรกฎาคม 2559 ลดลง 0.4841 บาทต่อกิโลกรัม จาก 15.4542 บาทต่อกิโลกรัม เป็น 14.9701 บาทต่อกิโลกรัม (2) คงต้นทุนโรงกลั่นน้ำมันเชื้อเพลิงและโรงอะโรเมติก อ้างอิงราคาตลาดโลกที่ CP-20 เหรียญสหรัฐฯ ต่อตัน เนื่องจากเป็นต้นทุนที่เหมาะสม ซึ่งจะทำให้ราคาก๊าซ LPG จากโรงกลั่นน้ำมันเชื้อเพลิงฯ เดือนพฤษภาคม 2559 อยู่ที่ 11.5294 บาท

ต่อกิโลกรัม (3) คงต้นทุนก๊าซ LPG จากการนำเข้าอยู่ที่ CP + 85 เหรียญสหรัฐฯต่อตัน ทำให้ต้นทุนการนำเข้า

ก๊าซ LPG เดือนพฤษภาคม 2559 อยู่ที่ 15.2315 บาทต่อกิโลกรัม และ (4) ต้นทุนบริษัท ปตท.สผ.สยาม จำกัด เดือนพฤษภาคม – กรกฎาคม 2559 อยู่ที่ 15.10 บาทต่อกิโลกรัม จากราคาก๊าซ LPG ตลาดโลก (CP)

เดือนพฤษภาคม 2559 อยู่ที่ 347 เหรียญสหรัฐฯต่อตัน ปรับตัวเพิ่มขึ้นจากเดือนเมษายน 2559 จำนวน 15 เหรียญสหรัฐฯต่อตัน และอัตราแลกเปลี่ยนเฉลี่ยเดือนเมษายน 2559 อยู่ที่ 35.2582 บาทต่อเหรียญสหรัฐฯ แข็งค่าขึ้นจากอัตราแลกเปลี่ยนเฉลี่ยเดือนมีนาคม 2559 จำนวน 0.1449 บาทต่อเหรียญสหรัฐฯ ส่งผลให้ราคา ณ โรงกลั่น ซึ่งเป็นราคาซื้อตั้งต้นของก๊าซ LPG (LPGPool) ปรับลดลง 0.1196 บาทต่อกิโลกรัม จากเดิม 14.0285 บาท

ต่อกิโลกรัม มาอยู่ที่ 13.9089 บาทต่อกิโลกรัม

2. กบง. เมื่อวันที่ 3 กุมภาพันธ์ 2559 มีมติให้ยกเลิกการชดเชยค่าขนส่งทุกคลังทั่วประเทศ โดยให้มีบัญชีค่าขนส่งก๊าซ LPG ไปยังคลังต่างๆ ประกอบการกำกับดูแลราคา ณ คลังภูมิภาค เพื่อให้กระทรวงพาณิชย์ใช้เป็นข้อมูลควบคุมราคาขายปลีกก๊าซ LPG เพิ่มขึ้นจากเดิมได้ไม่เกินไปกว่าอัตราค่าขนส่งที่ระบุไว้ในบัญชีค่าขนส่งต่อไปอีกเป็นเวลา 3 เดือน (พฤษภาคม-กรกฎาคม 2559) เพื่อให้ผู้ประกอบการที่รับก๊าซจากคลังภูมิภาคที่เคยได้รับการชดเชยมีเวลาในการปรับตัว

3. กบง. เมื่อวันที่ 30 มีนาคม 2559 รับทราบเรื่องแนวทางการเปิดเสรีธุรกิจก๊าซ LPG ซึ่งปัจจุบัน

มีความก้าวหน้าในการดำเนินการ ดังนี้ (1) การกำหนดอัตราค่าบริการการใช้คลัง/ท่าเรืออยู่ในระหว่างการจัดทำอัตราค่าบริการคลังที่เหมาะสม และนำเสนอต่อ กบง. (2) การออกระเบียบหลักเกณฑ์การใช้คลัง/ท่าเรือ บริษัท ปตท. จำกัด (มหาชน) ได้จัดทำร่างระเบียบเบื้องต้นแล้ว และอยู่ระหว่างรอการพิจารณาร่วมกับหน่วยงานที่เกี่ยวข้อง (3) การออกระเบียบการคัดเลือก/ประมูล กรมธุรกิจพลังงาน อยู่ระหว่างการจัดทำระเบียบการคัดเลือก และนำระเบียบดังกล่าวไปทำการรับฟังความคิดเห็นจากกลุ่มโรงกลั่นน้ำมัน และกลุ่มผู้ค้าก๊าซ LPG และ (4) การดำเนินการคัดเลือก/ประมูล

ยังไม่ได้ดำเนินการ

4. จากราคาก๊าซ LPG Pool ของเดือนพฤษภาคม 2559 ที่ปรับตัวลดลง 0.1196 บาทต่อกิโลกรัม และเพื่อเป็นการลดภาระการชดเชยของกองทุนน้ำมันฯ ฝ่ายเลขานุการฯ จึงได้เสนอให้คงราคาขายปลีกก๊าซ LPG ไว้ที่ 20.29 บาทต่อกิโลกรัม โดยปรับลดการชดเชยกองทุนน้ำมันฯ ลง 0.1196 บาทต่อกิโลกรัม จากเดิมกองทุนน้ำมันฯ ชดเชยที่ 0.7095 บาทต่อกิโลกรัม เป็นกองทุนน้ำมันฯ ชดเชยที่ 0.5899 บาทต่อกิโลกรัม ส่งผลให้กองทุนน้ำมันฯ มีรายจ่ายประมาณ 213 ล้านบาทต่อเดือน โดยฐานะกองทุนน้ำมันเชื้อเพลิงก๊าซ LPG ณ วันที่ 1 พฤษภาคม 2559 มีฐานะกองทุนสุทธิ 7,623 ล้านบาท และเพื่อให้ผู้ประกอบการที่รับก๊าซ LPG จากคลังภูมิภาคที่เคยได้รับการชดเชยมีเวลาในการปรับตัว ฝ่ายเลขานุการฯ จึงได้เสนอให้มีบัญชีค่าขนส่งก๊าซ LPG ไปยังคลังต่างๆ ประกอบการกำกับดูแลราคา

ณ คลังภูมิภาค ต่อไปอีกเป็นเวลา 3 เดือน (พฤษภาคม-กรกฎาคม 2559) และเพื่อให้กรมธุรกิจพลังงาน (ธพ.) สำนักงานนโยบายและแผนพลังงาน (สนพ.) และ ปตท. มีระยะเวลาเตรียมการด้านเอกสารและระเบียบต่างๆ อย่างรอบคอบ เห็นควรปรับกรอบระยะเวลาเตรียมการ การดำเนินงานตาม “Roadmap การเปิดเสรีธุรกิจก๊าซ LPG” ให้มีความยืดหยุ่นมากยิ่งขึ้น จากเดิมที่กำหนดให้นำเสนอ กบง. เกี่ยวกับหลักเกณฑ์การเปิดเสรีธุรกิจก๊าซ LPG ภายใน

ต้นเดือนมิถุนายน 2559 ให้เป็นเสนอ กบง. ภายในเดือนมิถุนายน – กรกฎาคม 2559

มติของที่ประชุม

1. เห็นชอบการกำหนดราคาต้นทุนจากแหล่งผลิตและแหล่งจัดหา ดังนี้

1.1 กำหนดราคาก๊าซ LPG ที่ผลิตจากโรงแยกก๊าซธรรมชาติ ณ ระดับราคา 14.9701 บาทต่อกิโลกรัม

1.2 กำหนดราคาก๊าซ LPG ที่ผลิตจากโรงกลั่นน้ำมันและโรงอะโรเมติก เป็นราคาตลาดโลก (CP) ลบ 20 เหรียญสหรัฐฯต่อตัน

1.3 กำหนดราคาก๊าซ LPG จากการนำเข้า เป็นราคาตลาดโลก (CP) บวก 85 เหรียญสหรัฐฯต่อตัน

1.4 กำหนดราคาก๊าซ LPG ที่ผลิตจากบริษัท ปตท.สผ.สยาม จำกัด อำเภอลานกระบือ

จังหวัดกำแพงเพชร ณ ระดับราคา 15.10 บาทต่อกิโลกรัม

โดยที่ CP = ราคาประกาศเปโตรมิน ณ ราสทานูรา ซาอุดิอาระเบียของเดือนนั้น เป็นสัดส่วน ระหว่างโปรเปน กับ บิวเทน 60 ต่อ 40

ทั้งนี้ให้มีการทบทวนราคาต้นทุนจากแหล่งผลิตและแหล่งจัดหาทุกๆ 3 เดือน

2. เห็นชอบกำหนดอัตราเงินชดเชยสำหรับก๊าซ LPG ที่ผลิตในราชอาณาจักรกิโลกรัมละ 0.5899 บาท

3. เห็นชอบให้มีบัญชีค่าขนส่งก๊าซ LPG ไปยังคลังต่างๆ ประกอบการกำกับดูแลราคา ณ คลังภูมิภาคต่อไป

โดยมอบหมายให้สำนักงานนโยบายและแผนพลังงานรับไปดำเนินการออกประกาศคณะกรรมการบริหารนโยบายพลังงาน ทั้งนี้ให้มีผลบังคับใช้ตั้งแต่วันที่ 3 พฤษภาคม 2559 เป็นต้นไป

เรื่องที่ 2 แผนระบบรับส่งและโครงสร้างพื้นฐานก๊าซธรรมชาติเพื่อความมั่นคง

สรุปสาระสำคัญ

1. คณะรัฐมนตรีในการประชุมเมื่อวันที่ 30 มิถุนายน 2558 ได้มีมติเห็นชอบตามมติคณะกรรมการ นโยบายพลังงานแห่งชาติ (กพช.) เรื่อง แผนระบบรับ-ส่งและโครงสร้างพื้นฐานก๊าซธรรมชาติเพื่อความมั่นคง ดังนี้

(1) เห็นชอบโครงการลงทุนในระยะที่ 1 ของโครงข่ายระบบท่อส่งก๊าซธรรมชาติ จำนวน 3 โครงการ วงเงินลงทุนประมาณ 13,900 ล้านบาท โดยมอบหมายให้บริษัท ปตท. จำกัด (มหาชน) (ปตท.) เป็นผู้ดำเนินการ และ

(2) เห็นชอบในหลักการสำหรับการลงทุนในระยะที่ 2 และ 3 ของโครงข่ายระบบท่อส่งก๊าซฯ และโครงสร้างพื้นฐานเพื่อรองรับการจัดหา/นำเข้าก๊าซธรรมชาติ เหลว (LNG Receiving Facilities) โดยมอบหมายให้ ปตท. ไปดำเนินการศึกษารายละเอียดตามข้อเสนอแนะของคณะกรรมการกำกับกิจการพลังงาน (กกพ.) และให้นำผลการศึกษาเสนอต่อ คณะกรรมการบริหารนโยบายพลังงาน (กบง.) เพื่อพิจารณาให้ความเห็นชอบก่อนนำเสนอต่อคณะกรรมการนโยบายพลังงานแห่งชาติ (กพช.) เพื่อทราบต่อไป

2. ต่อมาเมื่อวันที่ 27 ตุลาคม 2558 ครม. มีมติเห็นชอบตามมติ กพช. เรื่องแผนระบบรับส่งและโครงสร้างพื้นฐานก๊าซฯ เพื่อความมั่นคง ดังนี้ (1) เห็นชอบโครงการการลงทุนในระยะที่ 2 ของโครงข่ายระบบท่อส่งก๊าซฯ

(ส่วนที่ 1) โดยมอบหมายให้ ปตท. เป็นผู้ดำเนินการ จำนวน 2 โครงการ วงเงินรวม 110,100 ล้านบาท (2) เห็นชอบให้เลื่อนโครงการลงทุนในระยะที่ 3 ของโครงข่ายระบบท่อส่งก๊าซฯ (ส่วนที่ 1) ออกไป 6-10 ปี ประกอบด้วยโครงการสถานีเพิ่มความดันก๊าซฯ จำนวน 2 โครงการ (ส่วนที่ 1 ระยะที่ 3) วงเงินรวม 12,000 ล้านบาท (3) ในส่วนของการลงทุน LNG Receiving Facilities (ส่วนที่ 2) จำนวน 2 โครงการ วงเงินรวม 65,500 ล้านบาท มอบหมายให้ กระทรวงพลังงาน โดยสำนักงานนโยบายแลพแผนพลังงาน (สนพ.) กรมเชื้อเพลิงธรรมชาติ (ชธ.) ร่วมกับ กกพ. และ การไฟฟ้าฝ่ายผลิตแห่งประเทศไทย (กฟผ.) ไปศึกษาเพิ่มเติมโดยให้คำนึงถึงแนวโน้มความต้องการใช้ก๊าซฯ ในอนาคตอย่างใกล้ชิด แล้วนำกลับมาเสนอ กบง. และ กพช. ตามลำดับอีกครั้ง

3. ในช่วงปี 2558 จนถึงปัจจุบัน มีโครงการโรงไฟฟ้าถ่านหินบางโครงการมีแนวโน้มที่จะไม่สามารถดำเนินการให้แล้วเสร็จได้ตามกำหนดการที่ระบุไว้ในแผน PDP 2015 ประกอบกับในช่วงปลายปี 2558 ที่ผ่านมา

เกิดวิกฤตการณ์ราคาน้ำมันตลาดโลกตกต่ำซึ่งส่งผลให้ราคาก๊าซฯ ทั้งในประเทศและในตลาดโลกมีราคาลดลง

จนอยู่ในระดับที่สามารถแข่งขันกับการผลิตไฟฟ้าโดยเชื้อเพลิงอื่นได้ ดังนั้นเพื่อลดความเสี่ยงด้านความมั่นคง กระทรวงพลังงานมีความจำเป็นต้องปรับเปลี่ยนแผนบริหารเชื้อเพลิงสำหรับผลิตไฟฟ้าในระยะสั้นและระยะกลาง

ให้สอดคล้องกับสถานการณ์ที่เปลี่ยนแปลงไป โดยมีแผนเพิ่มการใช้ก๊าซฯ ในการผลิตไฟฟ้าทดแทนโรงไฟฟ้าถ่านหิน

ที่อาจไม่สามารถดำเนินการได้ตามแผน PDP 2015 สรุปได้ดังนี้ (1) ความต้องการใช้ก๊าซฯ ในการผลิตไฟฟ้าที่ปรับเพิ่มสูงขึ้นจากกรณีฐาน (Base case) เนื่องจากจะมีการนำก๊าซฯ ไปใช้เป็นเชื้อเพลิงทดแทนการผลิตไฟฟ้าจากโรงไฟฟ้าถ่านหินที่ไม่สามารถดำเนินการได้ตามกำหนดการที่ระบุไว้ในแผน PDP 2015 รวมถึงโรงไฟฟ้าถ่านหินที่มีแนวโน้ม

จะดำเนินการล่าช้าจากกำหนดการตามแผน PDP 2015 กำลังผลิตติดตั้งรวมทั้งสิ้นประมาณ 3,340 เมกะวัตต์

(2) ความต้องการใช้ก๊าซฯ ในการผลิตไฟฟ้าที่ปรับเพิ่มสูงขึ้น จากการนำก๊าซฯ ไปใช้ในการผลิตไฟฟ้าทดแทนในกรณี

ที่แผน AEDP และ EEP ที่อาจจะสามารถดำเนินการตามเป้าหมายได้เพียงร้อยละ 70 ทั้งนี้ จากการนำก๊าซฯ

ไปใช้ในการผลิตไฟฟ้าทดแทนตามข้างต้น จะส่งผลให้ปริมาณความต้องการใช้ก๊าซฯ ในปี 2579 ปรับเพิ่มขึ้นจากกรณีฐานที่มีความต้องการใช้ก๊าซฯ อยู่ใน ระดับ 4,344 ล้านลูกบาศก์ฟุตต่อวัน ปรับเพิ่มขึ้นเป็นประมาณ 5,653

ล้านลูกบาศก์ฟุตต่อวัน

4. ตามแผนการจัดหาก๊าซฯ ของประเทศไทยในปัจจุบัน แบ่งการจัดหาออกเป็น 3 ส่วน ได้แก่

(1) จากแหล่งก๊าซฯ ภายในประเทศทั้งบนบกและในทะเล (อ่าวไทย) รวมถึงพื้นที่พัฒนาร่วมระหว่างประเทศ ผ่านทางระบบท่อส่งก๊าซฯ (2) นำเข้าก๊าซฯ จากแหล่งก๊าซฯ ในประเทศเพื่อนบ้าน (ประเทศเมียนมา) ผ่านทางระบบท่อส่งก๊าซฯ (3) นำเข้าในรูปแบบก๊าซฯ เหลว (LNG) ผ่านทาง LNG Receiving Terminal ทั้งนี้ในส่วนของการพิจารณาปรับแผนจัดหาก๊าซฯและ LNG ตามแผน Gas Plan 2015 นั้น ชธ. และ สนพ. ได้มีการพิจารณาโดยคำนึงถึงประเด็นความเสี่ยงในเรื่องของการบริหารจัดการแหล่งผลิตในอ่าวไทยที่สัมปทานจะสิ้นอายุลงในช่วงปี 2565 - 2566 โดยแบ่งออกเป็น 2 กรณี คือ กรณีที่สามารถบริหารจัดการให้สามารถคงกำลังการผลิตตามสัญญาได้ ซึ่งจะกำหนดให้เป็นกรณีฐานใหม่ และ กรณีไม่เป็นไปตามกรณีฐานซึ่งเป็นกรณีที่กระทรวงพลังงานไม่สามารถบริหารจัดการได้ ซึ่งจากแผนจัดหาก๊าซฯ ทั้ง 2 กรณี ชธ. และ สนพ. พบว่าในปี 2565 ประเทศจะมีความต้องการนำเข้า LNG ในปริมาณประมาณ 13.5 – 15.5 ล้านตันต่อปี และในช่วงปลายแผนในปี 2579 คาดว่าประเทศจะมีความต้องการนำเข้า LNG เพิ่มสูงขึ้นถึง 31.3 ล้านตันต่อปี ดังนั้นจึงมีความจำเป็นต้องมีการเตรียมความพร้อมโครงสร้างพื้นฐานเพื่อรองรับการนำเข้า LNG ให้มีความสามารถที่จะรองรับการนำเข้า LNG ในปริมาณดังกล่าวได้

5. เพื่อไม่ให้เกิดผลกระทบต่อความมั่นคงทางพลังงานในภาพรวมของประเทศ ควรมีการปรับแผนระบบรับส่งและโครงสร้างพื้นฐานก๊าซฯ เพื่อความมั่นคง ดังนี้ แผนเดิมตามมติครม. เมื่อวันที่ 30 มิถุนายน 2558 และ

27 ตุลาคม 2558 ส่วนที่ 1 โครงข่ายระบบท่อส่งก๊าซฯ จะยังไม่มีการปรับเปลี่ยนกรอบโครงการและสามารถดำเนินการต่อเนื่องต่อไปได้ และส่วนที่ 2 โครงสร้างพื้นฐานเพื่อรองรับการจัดหา/นำเข้าก๊าซธรรมชาติเหลว จะมีการปรับเปลี่ยนกรอบโครงการให้เหมาะสมกับสถานการณ์ความต้องการก๊าซฯ ที่เปลี่ยนแปลงไป ดังนั้น เพื่อให้โครงสร้างพื้นฐานก๊าซฯ ของประเทศเพียงพอและสอดคล้องกับแนวทางการจัดหาก๊าซฯ ฝ่ายเลขานุการฯ จึงได้เสนอให้พิจารณาปรับปรุงโครงการในส่วนที่ 2 ตามแผนระบบรับส่ง และโครงสร้างพื้นฐานก๊าซฯ เพื่อความมั่นคงให้มีความเหมาะสม โดยมีข้อสรุปเปรียบเทียบกับกรอบแผนเดิมที่ได้เคยนำเสนอต่อ กพช. และ ครม. แล้ว โดยแบ่งออกเป็น 2 กรณี

ดังนี้ (1) สำหรับรองรับการจัดหาก๊าซฯ ในกรณีฐานใหม่ การปรับเปลี่ยนโครงสร้างพื้นฐานในส่วนที่ 2 สำหรับรองรับนำเข้า LNG เพื่อให้สอดคล้องกับความต้องการใช้ก๊าซฯ ที่เพิ่มสูงขึ้น และการบริหารจัดการให้แหล่งผลิตในอ่าวไทยที่สัมปทานจะสิ้นอายุลงในช่วงปี 2565 - 2566 ยังคงสามารถผลิตต่อไปได้อย่างต่อเนื่อง และ (2) สำหรับรองรับการจัดหาก๊าซฯ ในกรณีที่ไม่เป็นไปตามกรณีฐาน การปรับเปลี่ยนโครงสร้างพื้นฐานในส่วนที่ 2 สำหรับรองรับการนำเข้า ก๊าซ LNG เพื่อให้สอดคล้องกับความต้องการใช้ก๊าซฯ ที่เพิ่มสูงขึ้น รวมทั้งรองรับการจัดหา LNG เพื่อทดแทนในกรณีที่กระทรวงพลังงานไม่สามารถบริหารจัดการแหล่งผลิตในอ่าวไทยที่สัมปทานจะสิ้นอายุลงในช่วงปี 2565 – 2566 ดังนั้น ฝ่ายเลขานุการฯ จึงได้ขอความเห็นชอบปรับเปลี่ยนโครงการ ดังนี้ (1) โครงการลำดับที่ 2.1 [T-1 ext.] : โครงการขยายกำลังการแปรสภาพ LNG ของ Map Ta Phut LNG Terminal เพิ่มเติมอีก 1.5 ล้านตันต่อปี วงเงินงบประมาณ 1,000 ล้านบาท โดยมอบหมายให้ บริษัท ปตท. จำกัด (มหาชน) เป็นผู้ดำเนินโครงการ มีกำหนดแล้วเสร็จสามารถนำเข้าและแปรสภาพ LNG จากของเหลวเป็นก๊าซเพื่อจัดส่งเข้าสู่โครงข่ายระบบท่อส่งก๊าซธรรมชาติ ในปี 2562 (2) โครงการลำดับที่ 2.2 [T-2] : โครงการ LNG Receiving Terminal แห่งใหม่ จ.ระยอง ในระยะที่ 1 สำหรับรองรับการนำเข้า LNG ในปริมาณ 5 ล้านตันต่อปี วงเงินงบประมาณ 36,800 ล้านบาท โดยมอบหมายให้ บริษัท ปตท. จำกัด (มหาชน) เป็นผู้ดำเนินโครงการ มีกำหนดแล้วเสร็จสามารถนำเข้าและแปรสภาพ LNG จากของเหลวเป็นก๊าซเพื่อจัดส่งเข้าสู่โครงข่ายระบบท่อส่งก๊าซธรรมชาติ ในปี 2565 ทั้งนี้ มอบหมายให้ บริษัท ปตท. จำกัด (มหาชน) ดำเนินการก่อสร้างเพื่อเตรียมความพร้อมของฐานรากทั้งหมดให้มีความพร้อมที่อาจสามารถขยายกำลังการแปรสภาพ LNG จากของเหลวเป็นก๊าซเพิ่มได้อีก 2.5 ล้านตัน (รวมกำลังการแปรสภาพ LNG สูงสุดเป็น 7.5 ล้านตันต่อปี) เพื่อรองรับความเสี่ยงหากเกิดการจัดหาก๊าซธรรมชาติไม่เป็นไปตามกรณีฐาน (3) โครงการลำดับที่ 2.4 [F-1] : โครงการ Floating Storage and Regasification Unit (FSRU) พื้นที่อ่าวไทยตอนบน สำหรับรองรับการนำเข้า LNG ในปีปริมาณ 5 ล้านตันต่อปี เพื่อจัดส่งก๊าซธรรมชาติให้แก่โรงไฟฟ้าพระนครใต้ พระนครเหนือ รวมทั้งจัดส่งก๊าซธรรมชาติเข้าสู่โครงข่ายระบบท่อส่งก๊าซธรรมชาติ โดยมอบหมายให้ กฟผ. เป็นผู้ดำเนินโครงการ ทั้งนี้

มอบให้ กฟผ. ไปศึกษาเพิ่มเติมถึงวงเงินลงทุนที่เหมาะสม เพื่อนำกลับมาเสนอต่อ กบง. และ กพช. พิจารณาให้

ความเห็นชอบต่อไป (4) โครงการลำดับที่ 2.3 [F-2] : โครงการ Floating Storage and Regasification Unit (FSRU) พื้นที่ อ.จะนะ จ.สงขลา หรือ อ.มาบตาพุต จ.ระยอง สำหรับรองรับการนำเข้า LNG ในปีปริมาณ 2 ล้านตันต่อปี เพื่อจัดส่งก๊าซธรรมชาติให้แก่โรงไฟฟ้าในเขตพื้นที่ ภาคใต้ของประเทศหรือบริเวณนิคมอุตสาหกรรมในภาคตะวันออกวงเงินงบประมาณ 27,000 ล้านบาท กำหนดแล้วเสร็จสามารถนำเข้าและแปรสภาพ LNG จากของเหลวเป็นก๊าซเพื่อจัดส่งก๊าซธรรมชาติให้แก่โรงไฟฟ้าได้ ในปี 2567 และมอบหมายให้ ชธ. และ กกพ. เตรียมความพร้อมในการเปิดประมูลคัดเลือกผู้ดำเนินโครงการต่อไป (5) โครงการลำดับที่ 2.5 [T-3] และ 2.6 [T-4 หรือ F-3] : โครงการ LNG Receiving Terminal ขนาด 3 ล้านตันต่อปี (ในกรณีของ F-3) ถึง 5 ล้านตันต่อปี เพื่อรองรับความต้องการใช้ก๊าซที่คาดว่าจะเพิ่มสูงขึ้นในอนาคต โดยมอบหมายให้ ชธ. กกพ. และ ปตท. ไปศึกษาเพิ่มเติม ทั้งในเรื่องสถานที่และวงเงินลงทุนที่เหมาะสม และให้มีการติดตามแนวโน้มความต้องการใช้ก๊าซธรรมชาติในอนาคตอย่างใกล้ชิด แล้วนำกลับมาเสนอ กบง. และ กพช. พิจารณาอีกครั้ง และ (6) โครงการที่ 2.3 [F-2] 2.5 [T-3] และ 2.6 [T-4 หรือ F-3] กำหนดให้การดำเนินโครงการต้องมีการออกประกาศเชิญชวนเพื่อคัดเลือกผู้ดำเนินโครงการ โดยมอบหมายให้ กกพ. เป็นผู้ดำเนินการกำหนดระเบียบและหลักเกณฑ์ในการคัดเลือกผู้ดำเนินโครงการ รวมถึงเป็นผู้คัดเลือกผู้ดำเนินโครงการที่เหมาะสม ทั้งนี้ให้เสนอผลการคัดเลือกผู้ดำเนินโครงการต่อรัฐมนตรีว่าการกระทรวงพลังงานเพื่อพิจารณาให้ความเห็นชอบต่อไปโดยมอบหมายให้ ชธ. และ กกพ. ติดตามแนวโน้มความต้องการใช้ก๊าซธรรมชาติในอนาคตอย่างใกล้ชิด

มติของที่ประชุม

1. เห็นชอบโครงการลำดับที่ 2.1 [T-1 ext.] : โครงการขยายกำลังการแปรสภาพ LNG ของ Map Ta Phut LNG Terminal เพิ่มเติมอีก 1.5 ล้านตันต่อปี วงเงินงบประมาณ 1,000 ล้านบาท โดยมอบหมายให้ บริษัท ปตท. จำกัด (มหาชน) เป็นผู้ดำเนินโครงการ มีกำหนดแล้วเสร็จสามารถนำเข้าและแปรสภาพ LNG จากของเหลว

เป็นก๊าซเพื่อจัดส่งเข้าสู่โครงข่ายระบบท่อส่งก๊าซธรรมชาติ ในปี 2562

2. เห็นชอบโครงการลำดับที่ 2.2 [T-2] : โครงการ LNG Receiving Terminal แห่งใหม่ จ.ระยอง

ในระยะที่ 1 สำหรับรองรับการนำเข้า LNG ในปริมาณ 5 ล้านตันต่อปี วงเงินงบประมาณ 36,800 ล้านบาท

โดยมอบหมายให้ บริษัท ปตท. จำกัด (มหาชน) เป็นผู้ดำเนินโครงการ มีกำหนดแล้วเสร็จสามารถนำเข้าและ

แปรสภาพ LNG จากของเหลวเป็นก๊าซเพื่อจัดส่งเข้าสู่โครงข่ายระบบท่อส่งก๊าซธรรมชาติ ในปี 2565 ทั้งนี้มอบหมายให้ บริษัท ปตท. จำกัด (มหาชน) ดำเนินการก่อสร้างเพื่อเตรียมความพร้อมของฐานรากทั้งหมดให้มีความพร้อมที่อาจสามารถขยายกำลังการแปรสภาพ LNG จากของเหลวเป็นก๊าซเพิ่มได้อีก 2.5 ล้านตัน (รวมกำลังการแปรสภาพ LNG สูงสุดเป็น 7.5 ล้านตันต่อปี) เพื่อรองรับความเสี่ยงหากเกิดการจัดหาก๊าซธรรมชาติไม่เป็นไปตามกรณีฐาน

3. เห็นชอบโครงการลำดับที่ 2.4 [F-1] : โครงการ Floating Storage and Regasification Unit (FSRU) พื้นที่อ่าวไทยตอนบน สำหรับรองรับการนำเข้า LNG ในปริมาณ 5 ล้านตันต่อปี เพื่อจัดส่งก๊าซธรรมชาติให้แก่โรงไฟฟ้าพระนครใต้ พระนครเหนือ รวมทั้งจัดส่งก๊าซธรรมชาติเข้าสู่โครงข่ายระบบท่อส่งก๊าซธรรมชาติ

โดยมอบหมายให้การไฟฟ้าฝ่ายผลิตแห่งประเทศไทยเป็นผู้ดำเนินโครงการ ทั้งนี้มอบให้การไฟฟ้าฝ่ายผลิตแห่งประเทศไทยไปศึกษาเพิ่มเติมถึงวงเงินลงทุนที่เหมาะสม เพื่อนำกลับมาเสนอต่อคณะกรรมการบริหารนโยบายพลังงาน (กบง.) และคณะกรรมการนโยบายพลังงานแห่งชาติ (กพช.) พิจารณาให้ความเห็นชอบต่อไป

ทั้งนี้ โครงการที่ 2.1 [T-1 ext.]2.2 [T-2] และ 2.4 [F-1] ให้นำเสนอ ต่อ กพช. เพื่อพิจารณาให้ความเห็นชอบต่อไป สำหรับโครงการที่ 2.3 [F-2] : โครงการ FSRU ในพื้นที่ภาคใต้ของประเทศ (พื้นที่ อ.จะนะ

จ.สงขลา หรือ อ.มาบตาพุต จ.ระยอง) 2.5 [T-3] : โครงการ LNG Receiving Terminal แห่งใหม่ (แห่งที่ 3) และ 2.6[T-4 หรือ F-3] : โครงการ LNG Receiving Terminal แห่งใหม่ (แห่งที่ 4) หรือ FSRU ที่ประเทศเมียนมาร์ มอบหมายให้สำนักงานนโยบายแลพแผนพลังงาน กรมเชื้อเพลิงธรรมชาติ คณะกรรมการกำกับกิจการพลังงาน และบริษัท ปตท. จำกัด (มหาชน) ไปศึกษาเพิ่มเติม แล้วนำกลับมาเสนอ กบง. เพื่อพิจารณาอีกครั้ง

สรุปสาระสำคัญ

1. เมื่อวันที่ 17 กันยายน 2558 กพช. ได้มีมติเห็นชอบแผนบริหารจัดการน้ำมันเชื้อเพลิง พ.ศ. 2558- 2579 (Oil Plan 2015) ตามที่กระทรวงพลังงานเสนอ พร้อมทั้งได้เสนอแนะว่าควรมีการทบทวนแผนฯ เมื่อมีการเปลี่ยนแปลงปัจจัยที่ส่งผลกระทบต่อเป้าหมายของแผนฯ อย่างมีนัยสำคัญ และให้หน่วยงานที่เกี่ยวข้องใช้ดำเนินการต่อไป โดยมอบหมายให้กรมธุรกิจพลังงาน รายงานความคืบหน้าการดำเนินงานตามแผนฯ ต่อ กบง. ทุก 3 เดือน และเมื่อวันที่ 3 กุมภาพันธ์ 2559 ธพ. ได้รายงานความคืบหน้าการดำเนินงานตามแผนฯ ไตรมาสที่ 1 (ตุลาคม – ธันวาคม 2558) ต่อ กบง. แล้ว

2. การจัดทำแผนบริหารจัดการน้ำมันเชื้อเพลิงเป็นการบูรณาการระหว่างแผนอนุรักษ์พลังงาน พ.ศ.2558 - 2579 กับแผนพัฒนาพลังงานทดแทนและพลังงานทางเลือก พ.ศ. 2558-2579 โดยเริ่มกระบวนการจัดทำแผนจากการพยากรณ์ปริมาณความต้องการใช้น้ำมันเชื้อเพลิง โดยตั้งอยู่บนพื้นฐานของข้อมูลปริมาณความต้องการใช้น้ำมันเชื้อเพลิงเดียวกับแผนอนุรักษ์พลังงาน ซึ่งได้มีการประเมินความต้องการใช้น้ำมันเชื้อเพลิงในกรณีฐาน (Business as Usual: BAU) ว่าในปี 2579 จะมีความต้องการใช้น้ำมันเชื้อเพลิงในภาคขนส่ง 65,459 ktoe โดยตามแผนได้กำหนดแนวทางมาตรการอนุรักษ์พลังงานในภาคขนส่ง โดยแบ่งแนวทางดำเนินการออกได้เป็น 4 กลุ่ม ได้แก่ (1) กำกับราคาเชื้อเพลิงในภาคขนส่งให้สะท้อนต้นทุนที่แท้จริง (2) เพิ่มประสิทธิภาพการใช้เชื้อเพลิงในยานยนต์ (3) ส่งเสริมการบริหารจัดการการใช้รถบรรทุกและรถโดยสาร และ (4) พัฒนาโครงสร้างพื้นฐานคมนาคมขนส่ง

3. จากข้อมูลการพยากรณ์ปริมาณความต้องการใช้น้ำมันเชื้อเพลิงดังกล่าว กรมธุรกิจพลังงานจึงได้นำมาบริหารจัดการโดยกำหนดเป็นหลักการจัดทำแผน 5 มาตรการหลัก ดังนี้ (1) สนับสนุนมาตรการประหยัดน้ำมันเชื้อเพลิงในภาคขนส่งตามแผนอนุรักษ์พลังงาน พ.ศ. 2558 - 2579 (Energy Efficiency Plan: EEP 2015)

(2) บริหารจัดการชนิดของน้ำมันเชื้อเพลิงให้เหมาะสม (3) ปรับโครงสร้างราคาน้ำมันเชื้อเพลิงให้เหมาะสม

(4) ผลักดันการใช้เชื้อเพลิงเอทานอลและไบโอดีเซล ตามแผนพัฒนาพลังงานทดแทนและพลังงานทางเลือก

พ.ศ. 2558 -2579 (Alternative Energy Development Plan: AEDP2015) (5) สนับสนุนการลงทุนในระบบโครงสร้างพื้นฐานน้ำมันเชื้อเพลิง ซึ่งภายใต้ 5 มาตรการหลักดังกล่าวประกอบด้วยแผนงาน/โครงการ ทั้งสิ้น 46 โครงการ/กิจกรรม เช่น โครงการติดฉลากแสดงประสิทธิภาพพลังงานในยางรถยนต์ การพัฒนาระบบโครงสร้างพื้นฐานคมนาคมขนส่งรถไฟฟ้าขนส่งมวลชน ประชาสัมพันธ์สร้างความเชื่อมั่น และความเข้าใจเกี่ยวกับน้ำมัน

แก๊สโซฮอล์อี 20 และ อี 85 (ภายใต้โครงการส่งเสริมการใช้เชื้อเพลิงชีวภาพ) และโครงการศึกษาการใช้เชื้อเพลิงชีวภาพในการขนส่ง เป็นต้น

มติของที่ประชุม

ที่ประชุมรับทราบ

สรุปสาระสำคัญ

1. ตามคำสั่งคณะรักษาความสงบแห่งชาติที่ 120/2557 เรื่อง การปรับโครงสร้างราคาน้ำมันเชื้อเพลิง

ลงวันที่ 28 สิงหาคม 2557 โดยการปรับภาษีสรรพสามิตและกองทุนน้ำมันเชื้อเพลิงทำให้ราคาขายปลีกเปลี่ยนแปลงไป ซึ่งผู้ค้าน้ำมันจะได้รับเงินชดเชยหรือส่งเงินเข้ากองทุนน้ำมันฯ ตามปริมาณน้ำมันคงเหลือของวันที่

28 สิงหาคม 2557 คูณด้วยอัตราเงินชดเชยหรืออัตราเงินส่งเข้ากองทุนน้ำมันฯ ที่ สนพ. ประกาศ ทั้งนี้ตามคำสั่งฯ กำหนดให้กรมธุรกิจพลังงาน (ธพ.) และสำนักงานพลังงานจังหวัดแจ้งเป็นหนังสือให้ผู้ค้าน้ำมันในพื้นที่ที่รับผิดชอบทราบจำนวนเงินชดเชยที่พึงได้รับหรือจำนวนเงินส่งเข้ากองทุนน้ำมันฯ (หนังสือให้ผู้ค้าฯ) เพื่อให้ผู้ค้าน้ำมันยื่นเอกสารขอรับเงินชดเชยหรือส่งเงินเข้ากองทุนน้ำมันฯ ต่อสถาบันบริหารกองทุนพลังงาน (องค์การมหาชน) (สบพน.) ทราบภายใน 90 วัน นับแต่วันที่ได้รับหนังสือจากพลังงานจังหวัด

2. เมื่อวันที่ 25 พฤษภาคม 2558 บริษัท ซัสโก้ จำกัด (มหาชน) ได้มีหนังสือถึง สบพน. แจ้งว่าบริษัท

ซัสโก้ฯ ไม่ได้รับหนังสือให้ผู้ค้าฯ จากสำนักงานพลังงานจังหวัดสระบุรี (พนจ. สระบุรี) ในเวลาอันควร ทำให้บริษัท

ซัสโก้ฯ ไม่ได้ดำเนินการขอรับเงินชดเชยจากกองทุนน้ำมันฯ มาก่อนหน้านี้ จึงขอยื่นเอกสารขอรับเงินชดเชยจากกองทุนน้ำมันฯ จากการปรับราคาขายปลีกสำหรับน้ำมันคงเหลือพร้อมแนบหนังสือให้ผู้ค้าฯ เป็นจำนวนเงิน 2,781,810.78 บาท ซึ่งต่อมา สบพน. ได้มีหนังสือถึง พนจ. สระบุรี เพื่อสอบถามข้อเท็จจริง โดย พนจ. สระบุรี

ได้ชี้แจงว่า พนจ. สระบุรี ได้ส่งมอบหนังสือให้ผู้ค้าฯ ให้กับพนักงานของบริษัทที่รับจ้างทำงานให้แทปไลน์ (พนักงาน Outsource) ซึ่งพนักงานคนดังกล่าวได้เดินทางไปรับหนังสือให้ผู้ค้าฯ และได้ส่งมอบเอกสารให้บริษัทผู้ค้าน้ำมัน

5 ราย คือ (1) บริษัท ซัสโก้ ดีลเลอร์ส จำกัด (2) บริษัท ไทยออยล์ จำกัด (มหาชน) (3) บริษัท เชฟรอน (ไทย) จำกัด (4) บริษัท เชลล์แห่งประเทศไทย จำกัด และ (5) บริษัท เอสโซ่ (ประเทศไทย) จำกัด (มหาชน) โดยตรงเรียบร้อยแล้ว ส่วนเอกสารของ บริษัท ซัสโก้ฯ ได้วางไว้บนโต๊ะทำงานของเจ้าหน้าที่ของ บริษัท ซัลโก้ฯ เนื่องจากเจ้าหน้าที่ไม่อยู่

ในห้องทำงาน

3. เมื่อวันที่ 10 สิงหาคม 2558 และวันที่ 3 ธันวาคม 2558 สบพน. ได้มีหนังสือถึง พนจ. สระบุรีเพื่อสอบถามว่า พนจ. สระบุรี ได้จัดส่งหนังสือให้ผู้ค้าฯ ให้แก่บริษัท ซัสโก้ฯ เมื่อใด และมีระเบียบวิธีการจัดส่งหนังสือให้ผู้ค้าฯ เป็นแบบใด ซึ่ง พนจ. สระบุรี ได้ชี้แจงว่า (1) เมื่อวันที่ 18 พฤษภาคม 2558 พนจ. สระบุรี ได้ส่งสำเนาหนังสือให้ผู้ค้าฯ ให้แก่บริษัท ซัสโก้ฯ ใหม่อีกครั้งในรูปแบบสำเนาเอกสาร เพื่อใช้แทนหนังสือให้ผู้ค้าฯ ตามที่บริษัท ซัสโก้ฯ อ้างว่ายังไม่ได้รับ และ (2) วิธีการจัดส่งเอกสารของ พนจ. สระบุรี ถ้าเป็นกรณีที่เป็นเอกสารทั่วไปจะให้ผู้ที่เกี่ยวข้องกับเอกสารสำคัญนั้น ติดต่อขอรับเอกสาร หรือจัดส่งเอกสารให้ทางจดหมายตอบรับ หรือไปส่งด้วยตนเอง แต่ถ้าเป็นกรณีการจัดส่งเอกสารเรื่องการขอรับเงินชดเชย เนื่องจากเป็นปีแรกที่ พนจ. สระบุรี เป็นผู้รับผิดชอบ สำนักงานได้ฝากส่งเอกสารให้กับเจ้าหน้าที่ของ พนักงาน Outsource

4. เมื่อวันที่ 19 พฤศจิกายน 2558 สบพน. ได้มีหนังสือถึงที่ปรึกษาคณะกรรมการสถาบันบริหารกองทุนพลังงาน (นายวันชาติ สันติกุญชร) เพื่อหารือข้อกฎหมายกรณีของบริษัท ซัสโก้ฯ ซึ่งที่ปรึกษาฯ ได้มีหนังสือ ตอบข้อหารือว่า การตีความเกี่ยวกับการปฏิบัติตามคำสั่งฯ อยู่ในอำนาจพิจารณาวินิจฉัยของ กบง. ตามข้อ 12 ของคำสั่งฯ ดังนั้น สบพน. ชอบที่จะรวบรวมข้อเท็จจริงส่งให้ กบง. พิจารณาดำเนินการวินิจฉัย ดังนั้น เมื่อวันที่ 23 กุมภาพันธ์ 2559 สบพน. ได้มีหนังสือถึง สนพ. ขอให้พิจารณาเสนอ กบง. พิจารณาวินิจฉัยกรณีบริษัท ซัสโก้ฯ ขอรับเงินชดเชยจากกองทุนน้ำมันฯ เกินระยะเวลา 90 วัน ซึ่ง สนพ. ได้พิจารณาจากข้อเท็จจริงทั้งหมดแล้ว และได้มีความเห็นให้

สบพน. พิจารณาดำเนินการจ่ายเงินชดเชยให้แก่บริษัท ซัสโก้ฯ เนื่องจากไม่ปรากฏหลักฐานทางข้อกฏหมายที่จะนำมาอ้างอิงสนับสนุนว่าบริษัท ซัสโก้ฯ ไม่ประสงค์ขอรับเงินชดเชย หากมีการฟ้องร้องดำเนินคดีจะมีผลเสียต่อไป

แต่เนื่องจาก สบพน. ได้ดำเนินการตรวจสอบข้อเท็จจริงจากหน่วยงานที่เกี่ยวข้องประกอบกับ ตามคำสั่งฯ ข้อ 12 ระบุว่า ในกรณีที่มีปัญหาในการตีความเกี่ยวกับการปฏิบัติตามคำสั่งนี้ ให้ กบง. พิจารณาวินิจฉัยและให้ถือว่าคำวินิจฉัยดังกล่าวเป็นที่สุด สบพน. จึงได้จัดทำข้อเสนอเพื่อให้ กบง. พิจารณาดำเนินการตามอำนาจหน้าที่ดังกล่าว

มติของที่ประชุม

มอบหมายให้สถาบันบริหารกองทุนพลังงานดำเนินการตรวจสอบหลักฐานและข้อเท็จจริงที่เกี่ยวข้องให้ครบถ้วน และให้พิจารณาดำเนินการตามระเบียบและคำสั่งที่เกี่ยวข้องว่าสามารถจ่ายเงินชดเชยจำนวน 2,781,810.78 บาท ให้แก่บริษัท ซัสโก้ ดีลเลอร์ส จำกัด ได้หรือไม่ และนำมารายงานให้คณะกรรมการบริหารนโยบายทราบต่อไป